When Labour Becomes Software

Disruption to the labour markets has been top of mind of late. Sharing Tapestry's take, this post evaluates the downstream effects from “The 4th Industrial Revolution” taking hold, centred around the below research from Goldman Sachs.

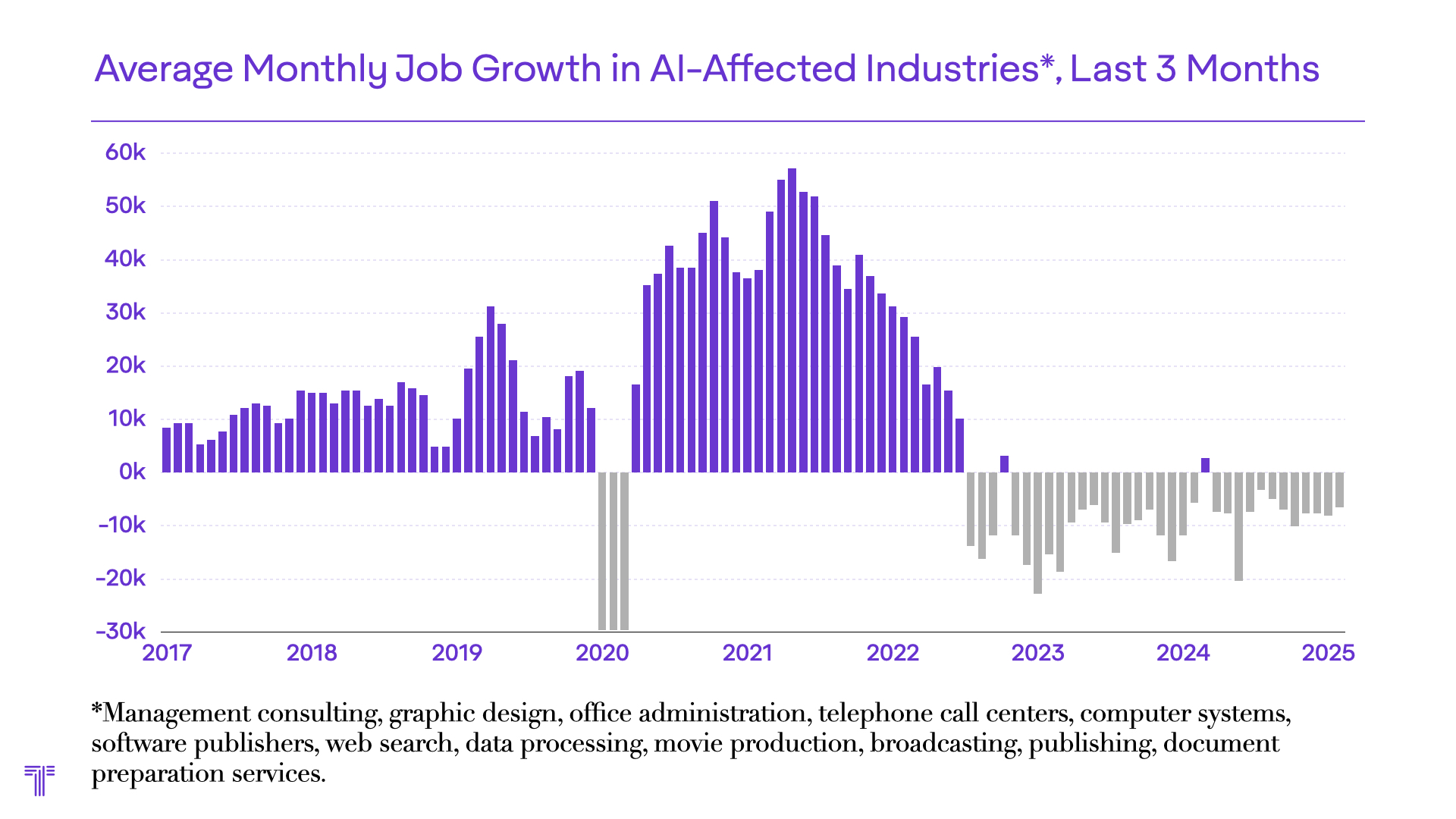

In category after category, nuanced work once delivered by people is being broken down into workflows, model calls, and token costs. The chart does not only surface the human impact, it is also a map of how underlying value is migrating.

This Goldman Sachs research points to early AI labour effects already being visible in a handful of knowledge-work niches - call centres, marketing and graphic design, and office administration - even if aggregate US employment data still shows little broad-based disruption.

In the bank's base case, 6-7% of workers could be displaced over roughly the next decade. And yet, only 9.3% of companies in one recent US survey actually had generative AI in production. This all makes the current moment notable: the effects are beginning to show up (see chart) before adoption is anything close to wide spread.

Another report, Anthropic's review of the labour-market, sharpens that picture. Its measure of "observed exposure" asks what LLMs are already doing in automated, work-related contexts, and weights API-like automation more heavily than casual augmentation.

On that measure, customer service representatives sit among the most exposed occupations (more below), alongside programmers and data-centric roles. Yet Anthropic have found no systematic increase in unemployment for highly exposed workers since late 2022. Combining these signals: hiring into, and movement between, exposed occupations has slowed.

Customer Service is One X-Ray

Dialling in on the customer service segment. The software layer is large: customer service software is estimated at $50B in 2025, with SaaS specifically accounting for 64% of that spend. But this is dwarfed by the service market as a whole, at c. $500B. So historically, the lionshare of value is not the per seat Enterprise software subscription. It is the human service layer sitting on top of the stack.

Anthropic's report captures the labour side of the same story: customer service representatives are now one of the most exposed occupations in the economy under its observed-exposure measure.

This is why the overhaul of customer support has become an "agentic arms race". Such categories are no longer defined by who can sell the most seats. They are now defined by who can absorb the most labour, safely, repeatedly, with a measurable outcome.

Producing the operating layer across multiple verticals

We see the same pattern across our portfolio.

Fin AI is a case in point. Across all customers, Fin now resolves an average of 67% of customer queries, and in Intercom's own support operation it resolves more than 81% of volume. It works not only inside Intercom, but across existing helpdesks like Zendesk and Salesforce. Our last newsletter set out a reformed pricing model that Intercom ushered in with Fin. They were a first-mover - we anticipate a wholesale shift from per seat to outcome pricing in the near-future.

Ichi is automating permitting with AI. Its platform can analyse more than one million building codes, automate QA/QC and submittal review, and answer complex code questions in under 20 seconds. That is specialised professional labour being rendered into software, with the human reviewer moving from repetitive checking towards higher-order judgement.

Sunrise Robotics is the physical-world mirror. Tapestry describes the company as part of a software-led transformation in manufacturing, and Sunrise frames their mission as augmenting humanity through intelligent robotics. Its autonomous robotic cells are designed to let manufacturers redeploy operators towards their highest-value work. This is not a story about labour disappearing in one step. It is a story about repetitive labour becoming machine-executable.

Augmentation > Redundancy

At this point we part ways with both the optimists and the catastrophists. The zero to one take of the medium-term outcome is not mass overnight replacement. Anthropic explicitly warns that AI's labour effects may end up looking less like the Covid shock and more like the internet or the China-trade shock: slower, noisier, and harder to isolate in aggregate data. So far, that is exactly what the evidence suggests.

In customer service, the operating model emerging today is hybrid. Capgemini finds that consumers still overwhelmingly prefer human agents for empathy and creative problem-solving, and concludes that the future lies in a blend of human and virtual agents. Intercom reports the same organisational shift from inside the category: 45% of support teams have already updated job descriptions to include AI-related responsibilities; 40% say their human agents now spend more time training AI systems; and 27% say people are increasingly focused on complex escalations and edge cases. The human-in-the-loop becomes less operative and more supervisory.

That said, it would be naive to assume the ladder beneath the profession remains intact. The most worrying signal in the Anthropic report is not mass unemployment among tenured workers. It is the friction appearing at the entry point. If the young find it materially harder to land their first role in exposed occupations, then AI may break the apprenticeship path, resulting in structural discontinuity across sectors.

Where Does the Upended Value Land?

Augmented or Redundant - the supplanting of human-labour with agentic capabilities presents substantial economic opportunity. The implied personnel value of these sectors could be distributed three-ways.

Growth & Productivity, at the forefront of technological advancements. Efficient markets will re-price augmented services, with end-users streamlining processes and lowering overheads.

Infrastructure, the explosion of token-hungry agents across our systems are, for now at least, cost-constrained. Critical resources including compute, GPU chips and the downstream structural inputs are each subject to scarcity. With a cost-line entrenched, and some exposure to shocks, the foundational infrastructure layer looks set to prop up token costs, for now.

Disruptors, Enterprise-grade actors able to win distribution and implement capabilities vertically stand to capture substantial upside. In customer service, that means the platform behind resolution. In manufacturing, it means the stack behind trained robots. In permitting, it means the structured knowledge, workflow, and governance layer that lets specialist judgement be prioritised.

The headline chart is therefore not just a warning about AI-affected hiring. It is the uprooting of value that has been entrenched in labour markets for time immemorial. For only the fourth time, that value is being redistributed.